Happy Story of Selling Houses

When I bought my first house, it was near the top of a housing cycle (not a bubble), so it was fairly expensive (but interest rates were still high as well). I got help getting a good down payment, I bought the house and then kind of forgot about its value for a year or two. Selling houses was nowhere in my mind at the time.

As time passed I started hearing about how little houses around us were selling for, and I became concerned, worried and a little depressed that I had effectively lost money by buying this house (we were already talking about needing to buy a bigger house).

We tried selling our house, but for 6 months there were no real offers (plenty of low ball 25% below asking price offers, which were ignored). We took the house off the market, but the next year the market started to pick up, so we actually were asking for what we had paid for the house (let’s called that value $N). After a lot of work, we finally did sell our house for pretty much exactly what we bought it for.

The following graph outlines the value of the house over time, but the fact that we bought and sold the house for the same amount (yes, we lost money on the deal due to closing costs and moving, let’s leave that out of the discussion for now).

I would say at point in time “Y“, I would say I was the most depressed about the price of my house, but from that point as I saw the house “increase in value“, I became much happier and thus when I sold I was very happy to get the price we got.

Unhappy Seller

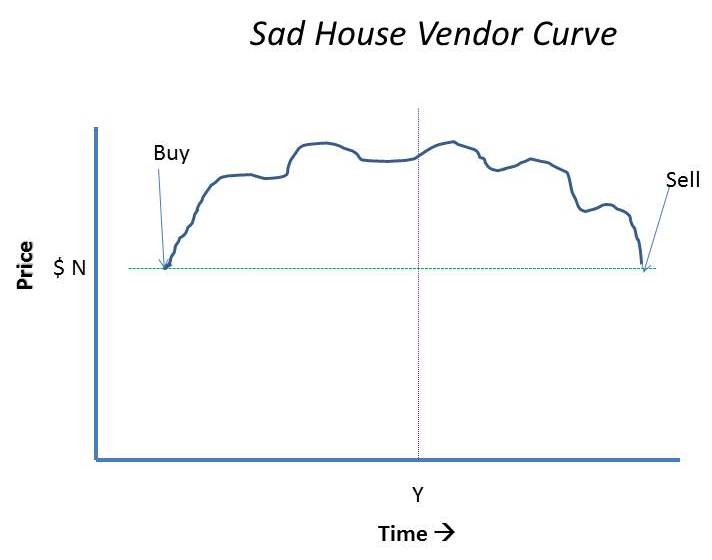

The house we bought when we sold our house seemed to have a much different story in terms of selling.

This house had been held for a long time, and had “appreciated” in value a great deal over time, but however, the owners weren’t looking to sell, so they felt very comfortable that their investment was appreciating in value.

Finally the owners decided to sell, because they were retiring, and they wanted to sell their house, however, at that time they were told that larger houses were not selling very well and they would have to lower their asking price (this depressed them greatly), and finally they sold the house (to my wife and I), for much less than they were asking, and about the same as what it cost them initially.

The following graph outlines their price odyssey:

Sad Vendor Price Graph

At point in time “Y”, this vendor was the happiest because their “investment” had gone up, but after that point they became more depressed because they were “losing” value in their house. I would say it would be safe to say that these vendors were unhappy about the price they received from the sale of this house.

Conclusions on Selling Houses

Here we have two house vendors, both received back what they put into their house, but because of the perceived value of their house, their relative happiness in the sale price was diametrically opposite, due to the perceived “gain” or “loss” of money (which they never had in the first place).

This is true with all “investments” what the relative value of something really doesn’t matter until you either (1) BUY or (2) SELL the investment. If you buy or sell your house because you perceive it is worth more and you want to “get my money now”, then that is fine but until you sell, the value of your house is unknown until it is sold.

My conclusions are simple: the only time the price of your house matters is when you sell it .

This is similar to the valuation of stocks….when I hear someone say my stocks of XXXX company are worth $$$$, using that valuation as part of their net worth — it’s only that price if they sell at that moment, with the same emotional rollercoaster ride when the prices fluctuate.

Precisely! It ain’t worth anything until you sell it!

I’d say the answer to your question is yes.

I generally don’t think of the house that I live in as an investment at all. Over the long term housing tracks the inflation. Houses, especially ones you are living in, are too expensive and difficult to buy and sell. The best thing to do is buy one house that meets your needs for at least 20 years or so and only move if you need to change locations.

If you need to move to a more expensive house, it is actually best to do it when the markets are down. Sure you get less for your current house but you also pay less for your new more expensive house, so you end up saving money. The reverse is true for downsizing.

Unless you downsize soon after buying your home and/or after a “bubble bursting”.

The big difference between the two graph, or rather the stories backing them, is the ability to control Y.

In the first scenario, you were able to simply wait out the period of lower value for your home. In the second scenario, well I’m not sure, but it seems like these folks were unable or unwilling to wait it out.

What if you had to sell early in the first scenario?

Ultimately, I mostly agree with your conclusion. Although, the value of your house does matter between buying and selling from a property tax perspective, but much less so.

True, but property taxes are the only tax on a “perceived value”, which really sucks (in my estimation).